Archive

The cost of Covid19 to HS2 – £1 Million a day

A friend of mine who works in insurance sent me the article below which I thought was interesting. It talks about the industry’s concerns about which clauses an insured might make a claim under due to Covid-19. It sounds like construction companies will have to pay extra for ‘disease extensions’ for policies in the future.

Has anyone had any insight yet as to what insurance companies are saying to your construction companies? With HS2 so large we’re looking at delay costs of around £1Million a day, the piling on my site is £30k a day alone and the insurance picture is unclear.

The Article

Vague construction wording could give rise to Covid-19 claims

The construction market is bracing for debate around Covid-19 claims as several wordings could be used by insureds to make a claim, Insurance Insider understands.

London-based sources told this publication that there will inevitably be delays to projects currently underway – with some sources giving estimates of six months or more – meaning policies would have to be extended. New projects that were due to start have now been left in limbo due to the coronavirus crisis.

While it is too early for loss notifications, construction underwriters are scrutinising wordings which could leave them open to potential losses that would threaten the class’ recovering profitability.

“We are in totally uncharted territory. We are in survival mode, we have to just get through the next two to three months,” one source said.

Rates in the construction market had been going up by 20-35 percent following high loss activity and a number of exits over the past 18 months including Beazley, Brit, CNA Hardy and Talbot, with a range of others passing through remediation exercises.

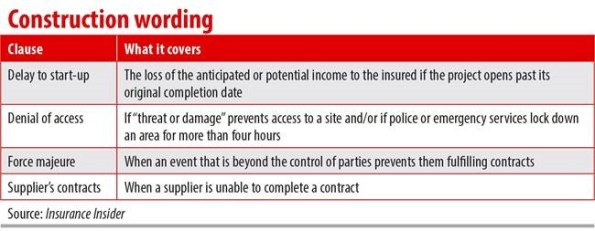

Delay to start up

One area currently under the microscope is a delay-to-start-up (DSU) clause, which is designed to cover the loss of the anticipated or potential income to the insured if the project opens past its original completion date.

However, sources told this publication that this clause’s trigger is typically physical loss or damage, and that it was not typical to have an infectious disease trigger, however the peril could be sub-limited.

One source added that, in the UK, infectious disease was a “standard or common” extension, so the UK may be disproportionately impacted.

Sources added that insureds typically have to wait until the scheduled completion date to make a claim, meaning there could be a time lag for claims.

Insureds can only claim under this DSU clause once, meaning they would have to buy this cover again – and possibly at an increased price.

Denial of access and force majeure

An additional area of concern is ingress or egress clause, otherwise known as denial of access. This wording could possibly warrant a payout, with one version of the clause implying that an insured could make a claim if there is a shutdown due to “threat or damage”.

Another version states that if emergency services or police have prevented access for more than four hours to a site, that could trigger a claim, even though it “wasn’t designed for this”, one source noted.

Force majeure wordings are also being examined by underwriters – where an event that is beyond the control of parties prevents them from fulfilling their contractual obligations.

Sources told this publication that, typically, force majeure events are specified in the construction contract, but some said coronavirus could be classed as a force majeure event, therefore making insurers liable.

There are various ways to invoke force majeure clause: a government mandate to cease construction, or prove that the coronavirus outbreak had caused one of the events on the list such as travel bans. The party would have to show that the events have impacted its ability to fulfil its obligations.

It was suggested that projects which relied on global supply chains were also struggling. This instance could be covered under all-risk or specific peril cover via suppliers’ contracts, but it is typically difficult to claim under, sources said.

Insurer actions

To combat uncertainty, insurers are introducing clarifications and exclusions on new business, but this is not universal across the sector.

“Some insurers are being slower than others to introduce the exclusions on new business. We are not looking to change existing contracts because that would be suicide; it would be stupid to go down that road. We are just looking at taking out disease extensions or making it clearer,” one source explained.

Overall, sources said the insurance sector was going through a “great period of uncertainty” and the picture globally was mixed, with some sectors stopping construction completely whereas others like the UK are allowing construction to go ahead.

Sources noted that risks were still getting bound and prices have gone up month on month for the past 12 to 18 months. This is set to continue, they added, and suggested it would be sensible for insureds to secure cover now before a potential price jump after the crisis.

There are still fears over the pipeline of new business as project financing is withdrawn by banks and lending is put on hold.

However, some underwriters were optimistic about stimulus packages, such as Donald Trump’s $2.2tn stimulus bill that was signed on Saturday, which could create jobs via new projects or infrastructure upgrades.